.avif)

Energy companies and manufacturers need to attract substantial investment — equity investments, loans, and tax credit monetization — to develop their projects. Historically, clean energy developers that wanted to monetize their tax credits had only one option: tax equity partnerships. While these partnerships have been instrumental in driving years of record US clean energy growth, they are not necessarily accessible for all developers and manufacturers or technology types. Tax equity partnerships are often limited to developers with portfolios of projects generating a large volume of tax credits.

Transferability has created new and more accessible ways for more developers and manufacturers — and more technology types, including advanced manufacturing, nuclear, and biogas — to monetize tax credits. With the emergence of transferability and the growth of this liquid and transparent transferable tax credit market, new financing structures have emerged.

Crux’s 2024 Transferable Tax Credit Market Intelligence Report explores these three structures and the trends emerging in how tax credit transfer deals are set up.

There are three main investment structures, each with its own unique ownership structure, indemnification characteristics, tax credit valuation, and treatment of depreciation:

Tax equity typically involves an equity investment structured as a partnership, which is made just prior to a project being placed in service. The investment helps substantiate a step-up in the project’s investment tax credit (ITC) basis to fair market value (FMV). In exchange, the tax equity investor usually receives substantially all the tax attributes, including depreciation, attributable to the project. After a period, the investor is typically bought out of the project.

Transferability has prompted many tax equity partnerships to evolve to allow for the sale of transferable credits to a third party. This happens in a transaction separate from the formation of the tax equity partnership and does not include the depreciation attributable to the project. The rise of these hybrid tax equity structures enabling the sale of tax credits in the transfer market has expanded tax equity funding for clean energy projects.

Some sellers elect to secure minority or preferred equity investments prior to selling their credits. These investments are arms-length transactions that occur prior to the project being placed in service and help substantiate an increase in the ITC basis to FMV. The developer then sells some or all the tax credits the project generates, and the investor typically benefits from a share of proceeds related to the tax credit sale. The developer can use some of the depreciation to offset the gain on sale of the interest to the new investor.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

In direct transfers, the project owner sells tax credits after they are generated. With ITCs, this can happen once a project is placed in service. Production tax credits (PTCs) can be sold after a project begins generating electricity or manufacturing an eligible product.

In direct transfers, the project’s owner is the seller. The project development company is often a pass-through entity, so buyers usually seek indemnities and assurances from the parent company to ensure the tax credits are eligible to be sold. The ITC's base value is linked to the project's cost basis because there's no arm's-length investment to increase it to FMV.

In this structure, no investment is required in the project. However, the project developer may secure a forward tax credit purchase commitment with a tax credit buyer, which can be used to obtain a bridge loan at relatively lower cost of capital compared to equity financing.

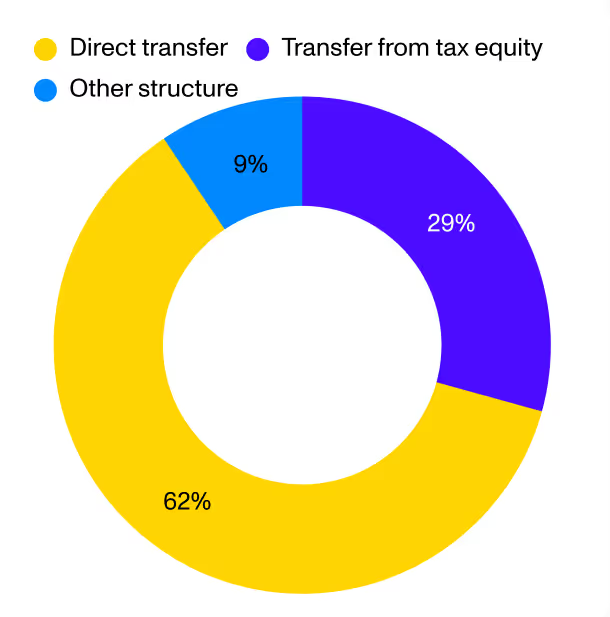

The 2024 market intelligence report — based on more than $25 billion in tax credit transaction data — found that transferability has had a profound effect on preferred investment structures:

Share of tax credits sold in transferable tax credit market by structure (current-year 2024 tax credits)

Crux also observed several other investment structure trends that emerged in 2024:

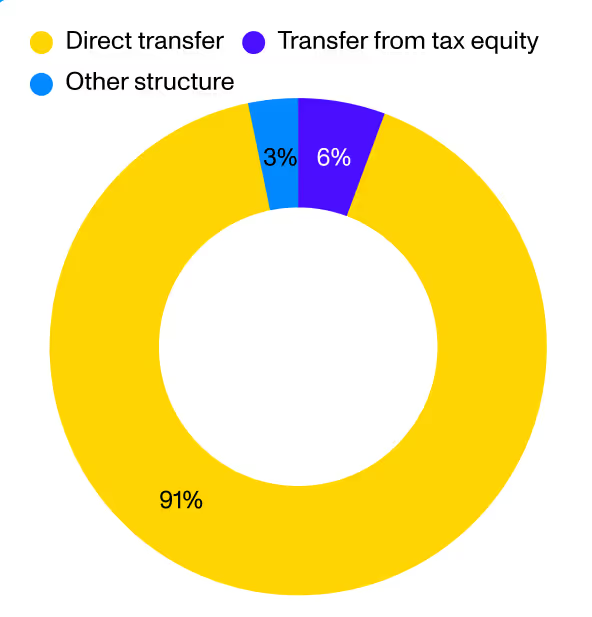

More than 90% of PTC sales originate as direct transfer deals where the project owner sells the credits. One reason: Recently eligible technologies including the §45X advanced manufacturing PTC and the §45U nuclear PTC do not lend themselves to tax equity investment structures. With traditional §45 PTCs, investments are underwritten with guaranteed 10-year access to PTC proceeds after a project is placed in service. With §45X and §45U, PTC availability is not tied to a facility being placed in service but rather when the tax credit is in effect in the law.

Seller structure for PTC deals, 2024

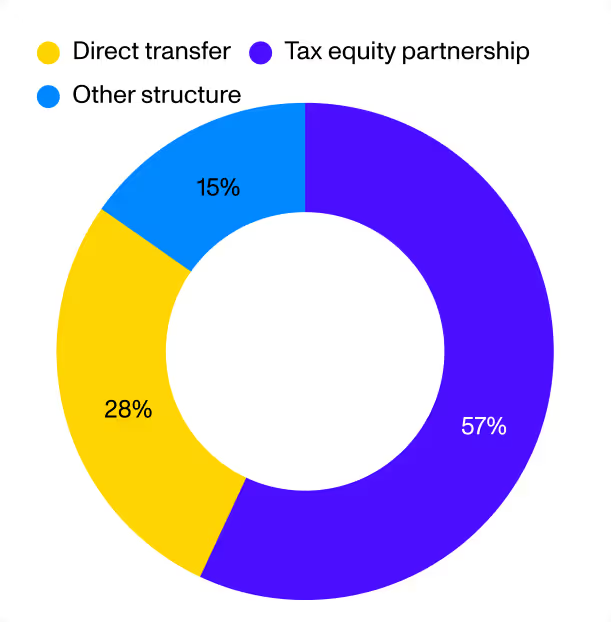

While PTCs sales are dominated by direct transfers, ITCs in 2024 embraced all three investment structures. Tax equity partnerships accounted for 57% of deal volume by gross market value. Direct transfers from developers made up 28% of deal volume, while 15% were preferred equity investment structures.

Seller structure for ITC deals, 2024

Projects that go directly to the transfer market disproportionately represent technologies that are newly eligible for the ITC, including large-scale energy storage, biofuels, and ITCs from advanced manufacturing projects. Standalone energy storage often has less access to the traditional tax equity market and is relatively more likely to be sold directly in the transfer market than to be financed through other investment structures. Biofuel projects, which were eligible for the §48 ITC through the end of 2024, nearly always sold tax credits directly from the seller.

The first §48C qualifying advanced energy projects also fell into the direct transfer category. §48C tax credits are allocated by the US Department of Energy (DOE) and the IRS out of an overall $10 billion total allocation. Projects that obtain these allocations are restricted insofar as how they can take on investors, making the use of tax equity impractical.

Preferred investment structures vary based on technology type, project size, and other factors. One common feature across deals, however, is the desire among buyers to indemnify their investments from any tax credit or transaction risk. Indemnification can come via the parent company of the tax credit sellers or through a third-party insurance policy.

Insurance is far more common with ITC deals. More than 75% of ITCs included either a full-wrap or partial insurance policy. PTCs are more likely to be indemnified by the tax credit seller. Only about 20% of PTC deals included insurance, and more than 80% were fully indemnified by the seller’s parent company. Only 2% of wind PTCs sold in 2024 included third-party insurance.

To learn more about trends in the 2024 transferable tax credit market, download the summary 2024 market intelligence report. The full report, which includes 20 additional pages of pricing data, is available for Crux platform users, survey participants, and partners. To receive a copy of the full report, get started on Crux.