Demand for energy is increasing for the first time in decades, and we urgently need more infrastructure to deliver affordable and reliable electricity. New infrastructure requires strong and secure domestic supply chains for minerals and components. Tax credits are the principal policy tool to achieve these two critical objectives and are key to U.S. competitiveness.

Investment in energy generation, manufacturing, and mining is accelerating, but project developers typically don’t have sufficient tax liability to use the tax credits they earn. To solve that problem, Congress made a dozen key tax credits transferable — unlocking a powerful new private sector market mechanism to catalyze investment in energy and manufacturing across the country. Leveraging the private sector to conduct appropriate due diligence and project management prevents fraud and ensures that infrastructure operates efficiently. Buyers and sellers in tax credit transfer deals have significant “skin in the game,” so they closely scrutinize transactions to ensure that the underlying tax credits are appropriately valued and claimed.

Crux’s research indicates that every dollar of federal tax credit drives five dollars of private sector investment. Transferable tax credits often unlock other forms of private sector financing, lowering capital costs. Credit buyers may also enter into other financial or commercial relationships with sellers, for instance, selling power alongside tax credit sales. The new market for transferable credits has quickly reached levels of efficiency and dynamism typically observed in more mature asset classes.

Transferability allows companies to sell tax credits to other companies for cash. The sale of credits reduces the cost of capital and allows developers and manufacturers to recycle capital more quickly. Companies that buy credits earn a small discount in exchange for the capital infusion and to reflect the diligence they perform. These private transactions take the place of grants or government refunds, which require the Internal Revenue Service (IRS) to directly arbitrate the provenance of a credit.

The ability to freely sell tax credits in a robust private market has several distinct advantages:

Over the coming decade, the U.S. economy will invest up to $1 trillion to power artificial intelligence (AI), cloud computing, and the resurgence of domestic manufacturing. Investors and lenders require a stable policy environment to deploy capital. Since 2022, developers and manufacturers have been afforded that stability by transferable tax credits that extend into the 2030s for a wide range of technologies. This new and successful policy provides additional powerful incentives to invest, build, and encourage growth and job creation.

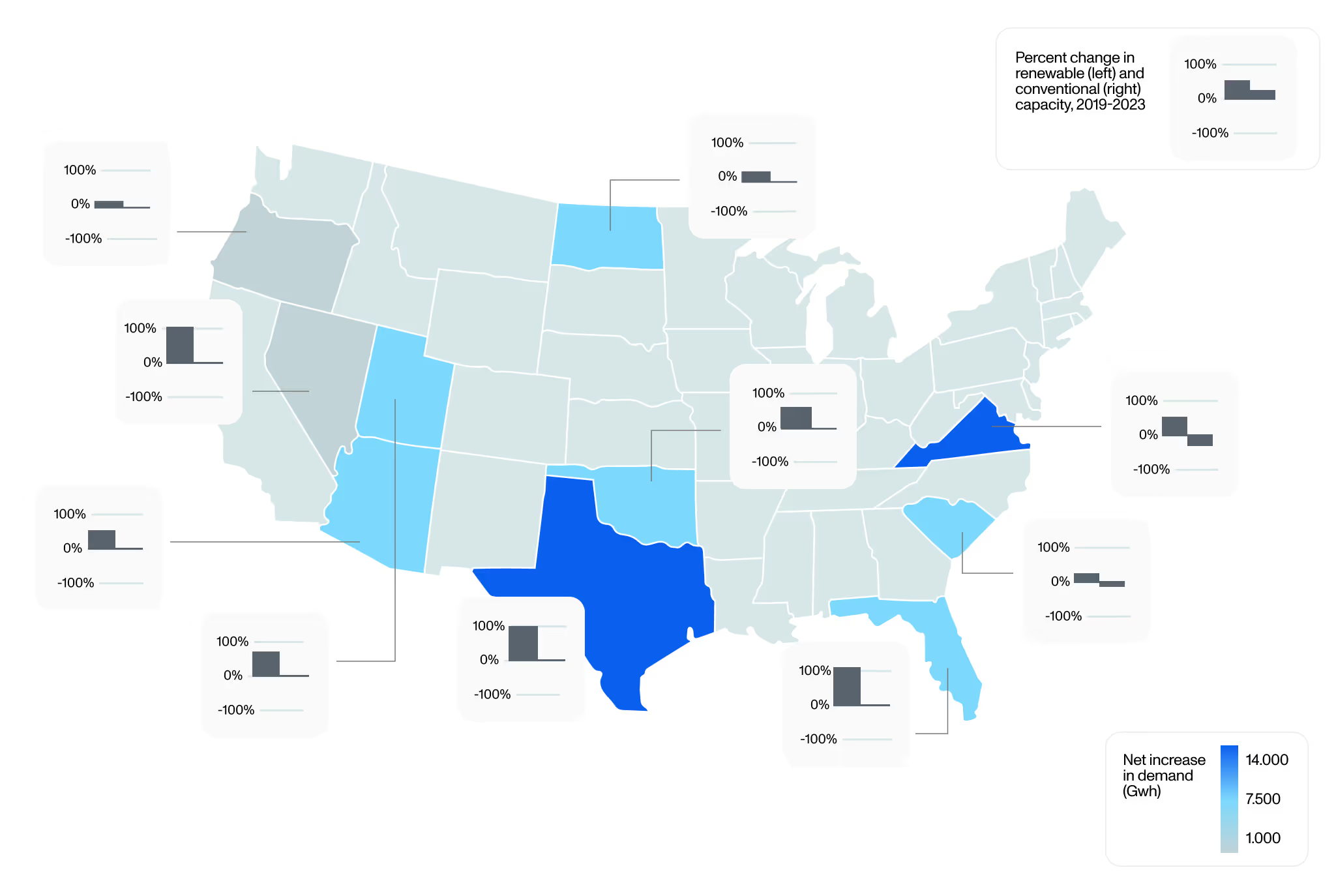

Tax credits — enabled by transferability — have already catalyzed more than $500 billion in private capital since 2022, on the basis of credit transfer deal volumes expected to reach $25 billion in 2024. The 10 states (below) with the most robust growth in electricity demand are also the states seeing the largest share of investment and the greatest proportion of transfer deals.

Ten states have seen rising electricity demand driven by the buildout of data centers, according to a U.S. Energy Information Administration (EIA) analysis of demand from 2019-2023. Commercial electricity demand in these states has risen by 10%, while demand in all other states fell 3% over the same time period. The states span the country and feature a diverse mix of energy resources, but they all have something in common: a substantial share of their power comes from wind, solar, energy storage, and nuclear power.

Map of states with rising energy demand and percent change in clean (left bar) and conventional (right bar) generation (2019-2023)

Across the 10 states with the highest rates of electricity demand growth, clean energy capacity has increased by 72% since 2019, adding nearly 70,000 MW of new energy generation. At the same time, conventional energy capacity declined by 150 MW. In the 40 states that are not experiencing the same pace of accelerated demand growth, clean energy capacity increased by 15%, or 29,000 MW, and conventional energy capacity declined 3%, by more than 14,000 MW.

Reliable and affordable energy depends on robust supply chains. The §45X advanced manufacturing production tax credit (PTC), introduced and made transferable by the Inflation Reduction Act (IRA), is driving historic investments in domestic manufacturing businesses. So far, data shows that battery supply chains are benefiting tremendously from the manufacturing boom catalyzed by this credit. The deep and dynamic market for §45X credits is driving historic investments in American manufacturing across 37 states, growing the economy, and enhancing U.S. security and competitiveness.

Tax credits are not effective if the company that earns the credits does not have sufficient near-term tax liabilities to use them. This is often the case with energy developers and manufacturers. Before transferability, developers relied on complicated financial transactions offered by a small group of large banks to monetize credits without directly selling them. This market — known as tax equity — was principally accessible to the largest developers of wind and solar projects, but little else.

The IRA provides credits for several new technology categories, including advanced manufacturing (§45X), nuclear (§45U), biofuels (§45Z), hydrogen (§45V), and standalone battery storage (§48). Many of these new credits are PTCs or have financing profiles that make tax equity inaccessible. Similarly, small and medium-sized businesses can access transferable credit marketplaces much more cost efficiently than was ever possible with tax equity.

Projects such as energy storage, domestic manufacturing facilities, and nuclear power plants also have unique operating characteristics and capital requirements that lend themselves to transferability rather than tax equity. Since 2022, when transferability was enacted into law, energy storage, manufacturing, and nuclear energy have become among the fastest-growing parts of the U.S. industrial economy.

Tax credit composition before (2022, left) and after (2024 YTD, right) transferability

Tax equity is generally provided by the largest banks to the largest developers. This capital has been expensive for all developers and generally inaccessible to small and mid-sized projects, or developers investing in new technologies and domestic supply chains. Deals are complex and can take more than six months to negotiate. Developers generally always incur hundreds of thousands, or even millions, of dollars in legal costs to secure tax equity.

All developers now have the option to sell credits in the transfer market — increasing access to capital and efficiency. Recent Crux data indicates that more than half of tax credit deals are for less than $50 million. In effect, the transfer market has created an efficient mechanism to raise capital for developers and manufacturers that typically wouldn’t have access to tax equity.

Crux has been proud to support dozens of credit transfers by projects that would not have had access to the traditional tax equity market. Among many other examples, these projects include expanded production lines at a solar manufacturer in Greenville, South Carolina; community solar projects in the rural Midwest; geothermal HVAC projects for multi-family housing; critical minerals mining, recycling, and refining in the U.S. Gulf; and utility-scale energy storage in Texas.

As Congress evaluates changes to the tax code in 2025, some have asked whether transferability might be restricted or removed. Such changes would have profound and cascading implications to energy and manufacturing projects across the country.

Presuming credits remained and transferability were removed, the market would revert to tax equity partnerships. Without transferability, only the largest wind and solar developers would have access to this capital.

Without the ability to access a liquid and transparent market for tax credits through transferability, we would see:

Transferability is driving the domestic energy and manufacturing renaissance. Consumers and businesses all across America benefit from this key innovation, which is making energy more affordable and abundant and securing our supply chains for generations to come.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.