The market for energy and manufacturing tax credits has seen immense growth in 2024. Total transaction volume for transferable tax credits is forecasted to reach $25 billion this year. In the third quarter alone, Crux estimates that $7-7.5 billion worth of tax credit deals closed, bringing the tally for the year to $18.5 billion as of September.

Crux is seeing an increasingly competitive market, especially for supply-constrained 2024 tax credits. Approximately 80% of the 2024 tax credits on Crux have already received a bid, and most are engaged with a buyer or have been sold. The remaining supply of tax credits is limited, and competition is becoming an unavoidable factor in tax credit deals. According to Crux’s Mid-Year Market Intelligence Report, more than 70% of tax credit deals in the first half of 2024 were sold through a competitive process.

As the market becomes more competitive, bid prices are converging across credits of different sizes and types. Our 3Q 2024 Market Update found limited price variance in tax credit pricing, indicating convergence in market price expectation among buyers. Sellers can expect the difference between the highest and lowest bids they receive to be about 4.0 cents for small credits, 1.2 cents for mid-sized credits, 0.5 cents for large credits, and 1.6 cents for mega deals.

Source: Crux 3Q 2024 Market Update

As competition increases and prices converge, sellers have more choices. Standing out is imperative for tax credit buyers. Although 91% of sellers report price is a key factor to optimize, they value a range of deal characteristics. Crux has identified several ways that buyers can help differentiate themselves and win in a competitive process:

Sellers indicate that readiness to transact is a key criteria they look for in a buyer. They don’t want to spend months engaged in contract negotiations. In many of the successful transactions that Crux has seen, sellers and tax credit buyers have aligned on transaction terms quickly, leading to a smoother due diligence and closing process. Advisors agree; more than 70% of advisors that Crux surveyed indicate that buyer education is the most important driver of a smooth transaction.

To improve their readiness to transact, buyers can make sure they’ve done internal education on:

Getting platform access to Crux to review listed credits can help all stakeholders understand the process.

Successful buyers have aligned internal stakeholders prior to approaching a deal. That can involve obtaining internal approval on their investment policy from their tax team, CFO, CEO, treasury, legal, and board (if necessary) prior to transacting. A clear investment policy includes elements related to credit type, size, pricing, credit support, and timing of payment.

If internal approval is not possible before transacting, buyers should have a clear outline of their internal approval process and the related timeline. Sellers will want to know that information when the parties are introduced, and having a plan in place will enable buyers to move quickly.

With internal alignment and approval on their tax credit strategy, buyers can set a saved search on the Crux platform for those criteria. Saved searches will immediately notify buyers of new credits fitting their criteria, so buyers can be the first to bid when a credit comes to market. Buyers should not hesitate to bid on multiple credits simultaneously, either; if multiple credits meet their criteria, there is no downside to bidding on multiple credits prior to exclusivity on a transaction.

Competition among buyers and the increasingly tight 2024 market are serving to accelerate transaction timelines, requiring that parties are prepared to move quickly once they are engaged. The faster buyers can produce a term sheet, the faster they can enter a period of exclusivity with the seller.

Buyers should start thinking about and involving relevant external parties, such as legal counsel, early. Understand accounting implications and coordinate with tax advisors. Select experienced tax credit counsel familiar with market standard forms and, as needed, a tax firm for additional diligence. Crux can always refer buyers to law firms and insurance brokers in its network.

Using standard documentation can also help increase readiness to transact and close faster-than-market deals — and save time and money on documentation drafting. Crux has the most market-validated standardized term sheet, due diligence checklist, and definitive documents in the market, based on market-vetted terms in collaboration with law firm partners that are highly experienced in tax credit transfers.

Consequently, closure within six weeks is more common on Crux than in the market — 66% of production tax credit (PTC) deals closed in that time frame (versus 44% in the market) and 32% of investment tax credit (ITC) deals (versus 19% in the market).

Buyers should also consider other factors that might make them attractive to sellers, including:

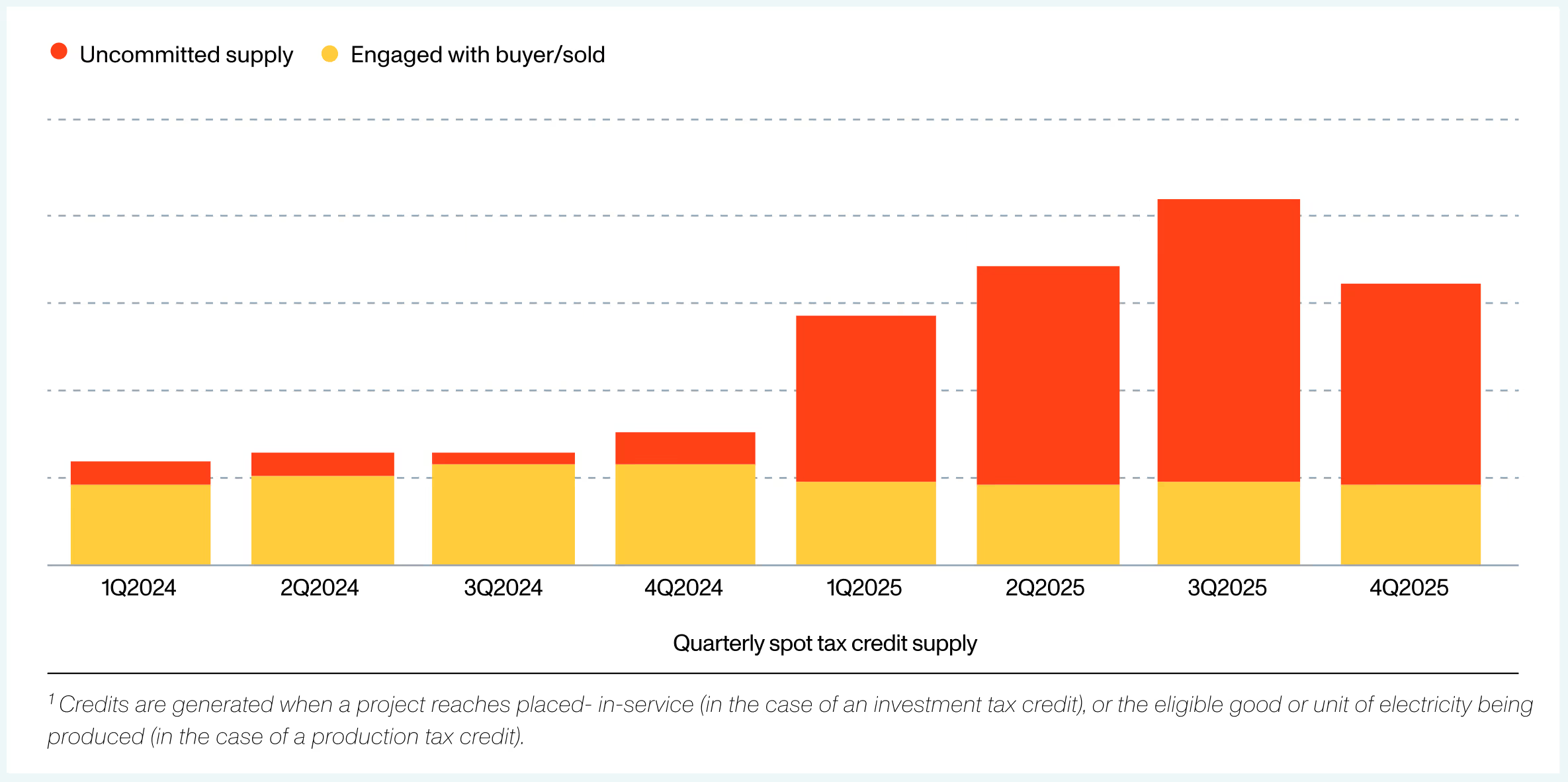

As the market for 2024 tax credits continues to grow more competitive, buyers are increasingly looking at forward commitments for 2025 (or later) tax credits. Buyers can commit to purchase tax credits in a future year, often at a discount to current-year spot market prices. IRS regulations require that tax credits be paid for in cash within the period beginning with the taxable year during which a credit is generated and ending on the due date for completing the transfer election statement, so commitments to purchase future tax credits do not involve immediate cash payment.

Including bids for multi-year PTC strips, 36% of bids on Crux in the third quarter of 2024 included a forward component. This represents a material increase from the second and first quarters, where bids for forwards represented 15% and 11% of all bid volume, respectively.

For tax credit buyers, forward commitments can provide an opportunity to engage with the widest market of tax credit sellers before most buyers are thinking about a future tax year. Crux has observed that the market for tax credits can become competitive relatively quickly and earlier than buyers might expect. By the third quarter of 2024, Crux found that 80% of credits listed by developers of the most liquid technologies (wind, solar, storage, 45X, 45U, and some renewable natural gas credits) receive bids within a week of listing.

Source: Crux 3Q 2024 Market Update

Tax credit sellers are often eager to engage buyers earlier. For sellers, lining up a forward commitment ahead of a project’s placed-in-service schedule (including during the construction phase or earlier) can provide the ability to access lower-cost financing solutions.

Buying tax credits? Increase your transaction readiness with Crux.

Crux has the largest supply of transferable tax credits and network of counterparties to support buyers. For more information on how to make your tax credit bid more efficient and competitive, get in touch with us.